Contribution margin is the amount of sales left over to contribute to fixed cost and profit. Contribution margin can be expressed in a number of different ways, including per unit and as a percentage of sales (called the contribution margin ratio). In the contribution margin income statement, we calculate total contribution margin by subtracting variable costs from sales. A contribution margin income statement reaches the same bottom-line result as a traditional income statement.

How do you calculate the contribution margin from EBIT?

It is useful to create an income statement in the contribution margin format when you want to determine that proportion of expenses that truly varies directly with revenues. The contribution margin income statement shown in panel B of Figure 5.7 clearly indicates which costs are variable and which are fixed. Recall that the variable cost per unit remains constant, and variable costs restaurant inventory guide for dummies in total change in proportion to changes in activity. Thus total variable cost of goods sold is $320,520, and total variable selling and administrative costs are $54,000. These two amounts are combined to calculate total variable costs of $374,520, as shown in panel B of Figure 5.7. Unlike a traditional income statement, the expenses are bifurcated based on how the cost behaves.

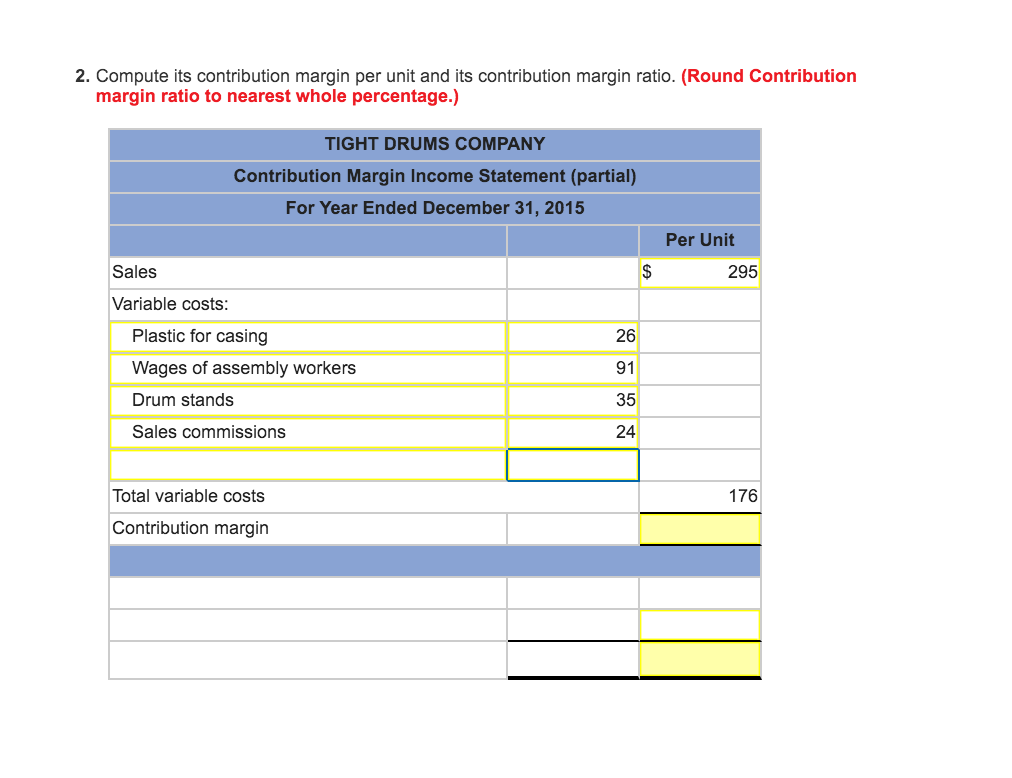

Contribution Margin Per Unit

In the case of XYZ Widgets Inc., a contribution margin of $300,000 and annual fixed costs of $100,000 would give a total income before tax of $200,000. In essence, if there are no sales, a contribution margin income statement will have a zero contribution margin, with fixed costs clustered beneath the contribution margin line item. As sales increase, the contribution margin will increase in conjunction with sales, while fixed expenses remain (approximately) the same.

Cost Behavior: Introduction to Fixed and Variable Costs

This is one of several metrics that companies and investors use to make data-driven decisions about their business. As with other figures, it is important to consider contribution margins in relation to other metrics rather than in isolation. The concept of contribution margin is applicable at various levels of manufacturing, business segments, and products.

- In its simplest form, a contribution margin is the price of a specific product minus the variable costs of producing the item.

- This format is called the contributionmargin format for an income statement because it shows thecontribution margin.

- This gives a much more detailed financial picture of the business’s operating costs and how well the products perform.

In this article, we shall discuss two main differences of two income statements – the difference of format and the difference of usage. Managers at ABC Cabinets would conclude from segment analysis that the fixtures segment is more profitable because it has a higher contribution margin. Using the formulas above, they could also see that the cabinet segment needs to generate almost double the sales compared to the fixtures segment to reach the break-even point. Because the direct costs of a segment are clearlyidentified with that segment, these costs are often controllable bythe segment manager.

Variable costs are not typically reported on general purpose financial statements as a separate category. Thus, you will need to scan the income statement for variable costs and tally the list. Some companies do issue contribution margin income statements that split variable and fixed costs, but this isn’t common. The contribution margin income statement is how you report each product’s contribution margin—a key part of smart operating expense planning.

Variable expenses are subtracted from sales to calculate the contribution margin. While the conventional income statement has its uses for external reporting functions, it is not as effective when used for internal reporting purposes. Traditional income statements do not differentiate between fixed and variable costs. The cost breakdowns shown in the contribution format income statements enable managers to see where they can control costs, make more-effective plans and reach critical decisions. For instance, XYZ Widgets Inc. can use the contribution format income statement to determine if most of their costs come from fixed or variable sources and how to reduce those costs.

This demonstrates that, for every Cardinal model they sell, they will have \(\$60\) to contribute toward covering fixed costs and, if there is any left, toward profit. Every product that a company manufactures or every service a company provides will have a unique contribution margin per unit. In these examples, the contribution margin per unit was calculated in dollars per unit, but another way to calculate contribution margin is as a ratio (percentage). The contribution margin income statement separates the fixed and variables costs on the face of the income statement. This highlights the margin and helps illustrate where a company’s expenses. Variable expenses can be compared year over year to establish a trend and show how profits are affected.